No Country for Economists

Is Turkey an interesting case of economic fluctuations? No. There is nothing mysterious about the slowdown in the Turkish economy. Anyone paying attention could and did see it coming miles away. All it took was a decline in the political stability, followed by the all too predictable decline in the quality of ministries’ decisions.

Is Turkey an interesting case of economic fluctuations? No. There is nothing mysterious about the slowdown in the Turkish economy. Anyone paying attention could and did see it coming miles away. All it took was a decline in the political stability, followed by the all too predictable decline in the quality of ministries’ decisions. The economy itself is not interesting the way, say, the American derivatives markets or London’s housing market is interesting to economists.

I remember the 1994 crisis, when the Turkish Lira depreciated around 50 percent. Why? Ms. Tansu Çiller - then prime minister - had cancelled treasury bond auctions and the lira’s liquidity was left to the market.

Absent a way to convince liquid investors to stay in the currency, the lira took a dive. Anyone with a vague notion of monetary policy could have predicted that. It’s like asking what will happen to a pressure cooker if you leave it on the oven too long. You don’t need a degree in chemistry to know that the thing is going to explode. Ms. Çiller happened to have a fancy American PhD in economics and it didn’t help her. It wasn’t about that.

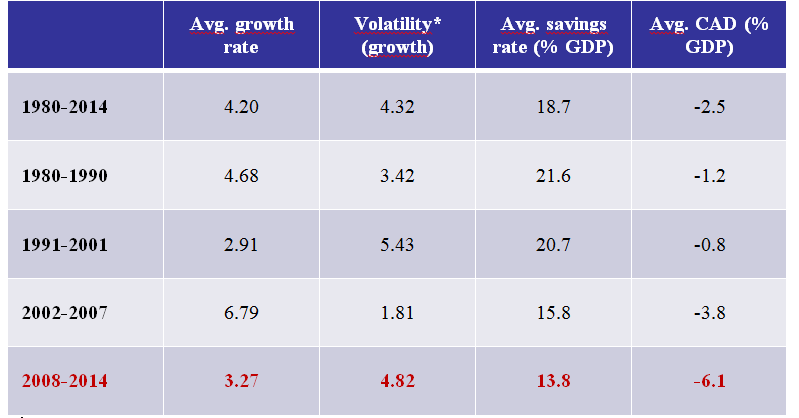

Think about the state of the economy today. Why is Turkey considered “fragile?” Right after 2008, as most other countries were trying to minimize their imbalances, Turkey did the opposite and its current account deficit skyrocketed. Just have a look at the numbers: compare the 2002-2007 period to 2008-2014. In the second period, the growth rate was halved down to 3.3 percent from 6.8 percent. Volatility of growth, on the other hand, has almost tripled. So with the global crisis, Turkey’s growth rate was not only halved, but also became very volatile. Why? Partly because in that second period, the current account deficit jumped up.

Turkey has a low savings rate and grows on high domestic demand, which makes it impossible to keep growing without running a deeper deficit. The result is that we now need to borrow more money per unit of economic growth. None of that is interesting in terms of economic analysis.

If – as is highly likely - the U.S. Fed decides to taper in the coming months, the era of easy money for countries like Turkey will end. The problem is that Turkey will still have a huge deficit going into this period.

I’ll spare you the fancy calculations to figure out what’s next: the lira will take a dive. Let me say it in different words. While waiting for the Fed’s decision, do you still have lively domestic demand to fuel growth?

Do you accelerate when you should be hitting the breaks? Then it’ll be the wall that stops you.

If it’s all so easy, you say, why not fix it? Because the problem isn’t with the economic machinery, it’s with the forces operating the levers. Without a political transition into a new status quo, there won’t be economic stabilization packages, no confidence in the markets and no structural reforms. Things will have to get worse before they get better. And the lira will fall.

Table 1. Growth rate, volatility, savings and current account deficit in Turkey (1980-2014)

*Standard deviation