Foreign investments inflow falls with deepening of political crisis

MUSTAFA SÖNMEZ

Tourists check currency exchange rates outside an currency exchange office in central Istanbul. Starting from May 2013, foreign investment inflow to countries such as Turkey, Brazil, South Africa and Indonesia started decreasing. REUTERS Photo

The month of May in 2013 was a critical month both for the world and the Turkish economy.After Dec. 17, 2013, the Turkish economy, in addition to the external winds, came under the effect of the political crisis that erupted with the Justice and Development Party (AKP) and the Gülen Community clash.

In such a case, how did the foreign investment inflow which has a vital importance for the Turkish economy, develop, what was the attitude of the foreigner who has short term investments and which direction did this affect the foreign currency prices, how will it affect them in the future? These questions are being asked and discussed almost every day.

The speech of FED Chairman Ben S. Bernanke in May 2013 on the “exit” plan of the United States, his indication that they would reduce monthly buying of bonds caused all the foreigners who had parked on “emerging” countries, in which Turkey is also included, to suddenly turn their faces to the United States.

Starting from May 2013, foreign investment inflow to countries such as Turkey, Brazil, South Africa and Indonesia started decreasing. It did not stop but its pace slowed down. This was immediately reflected in foreign currency prices and the dollar and the euro started gaining value rapidly.

Starting from May 2013, foreign investment inflow to countries such as Turkey, Brazil, South Africa and Indonesia started decreasing. It did not stop but its pace slowed down. This was immediately reflected in foreign currency prices and the dollar and the euro started gaining value rapidly.The Central Bank issued during the week the current accounts deficit November data.

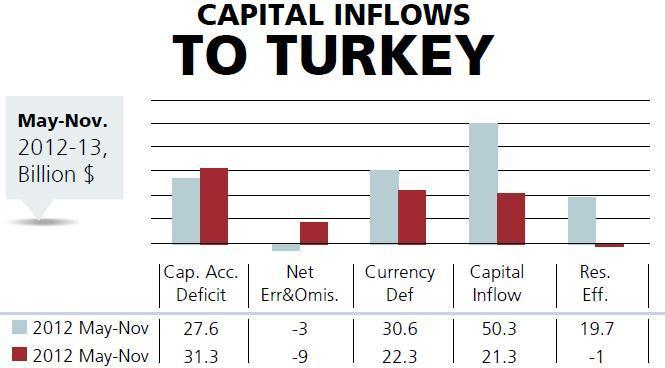

After taking this recent data into account, when we look at the foreign investment inflow, we can see that foreign investment inflow during the May-November period has been around $21 billion whereas this figure in the same period in 2012 has exceeded $50 billion. This signals a serious slowdown from 50 to 20.

The $50 billion of foreign resource that entered during the May-November period not only financed the current accounts deficit, it also strengthened and reinforced the foreign currency reserve. As a matter of fact, it can be seen that the inflow of foreign resources has contributed around $20 billion to the reserves in that time frame.

Whereas in the May-November 2013 period, we can see that this wind - the

same investment appetite - is continuing. In this period, the foreign

investment inflow was not able to cover the current accounts deficit

despite the government’s attempt to bring back the foreign exchange

reserves kept abroad (net error omission) that totaled $9 billion. Also a

reinforcement of $1 billion was needed from the reserve to finance the

deficit. This situation shows that there has been a significant slowdown

in the inflow of foreign investments and that gear 5 has gone down to

gear 2.

Whereas in the May-November 2013 period, we can see that this wind - the

same investment appetite - is continuing. In this period, the foreign

investment inflow was not able to cover the current accounts deficit

despite the government’s attempt to bring back the foreign exchange

reserves kept abroad (net error omission) that totaled $9 billion. Also a

reinforcement of $1 billion was needed from the reserve to finance the

deficit. This situation shows that there has been a significant slowdown

in the inflow of foreign investments and that gear 5 has gone down to

gear 2. At the beginning of May 2013, when the dollar was around 1.80 Turkish Liras, it first went up to 1.90 liras with the wind of FED and then to 2 liras and finally as 2013 was ending, it went up to 2.20 liras. The drop in the foreign investment inflow was indeed influential in this and it could be said that with the growth of the political crisis the problem will increase.

Foreign investors departed?

Meanwhile, on top of the domestic and international economic climate, did the change in the politic climate in Turkey with Dec. 17 accelerate the exit of the foreigners? Data shows that despite the decrease in the inflow of foreign investments, the foreigners have not yet emptied their portfolios and left.

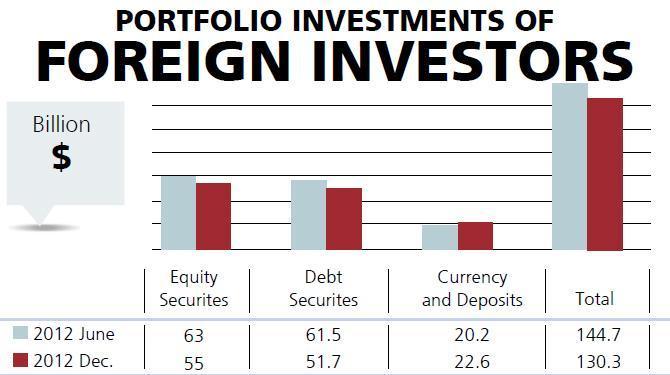

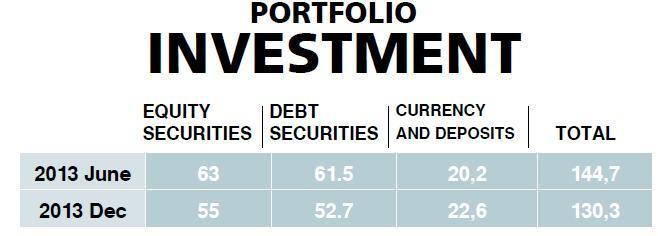

The total of the investments foreign investors did by converting their foreign currency into Turkish Liras and investing in shares and treasury bonds and those they deposited in banks was nearing $145 billion in June 2013.

During the rapid loss of the dollar, the value of the portfolios of the foreigners who could not leave the lira fell and when it was the end of 2013 the total of portfolio investments fell to $130 billion. This $15 billion drop should be interpreted as the melting down of the lira investments against the dollar’s valuation, not the exit of foreigners.

During the rapid loss of the dollar, the value of the portfolios of the foreigners who could not leave the lira fell and when it was the end of 2013 the total of portfolio investments fell to $130 billion. This $15 billion drop should be interpreted as the melting down of the lira investments against the dollar’s valuation, not the exit of foreigners. It is possible to say that the foreign investment inflow will further slow down with the flaming up, with the deepening of the political crisis; and that the short term investor will also depart by converting to dollars in the next relaxation of the exchange rate.

It could also be said that the current account deficit that has stayed at a certain amount despite the low growth, and also the obligation to pay $165 billion foreign debt in 12 months will increase the demand for foreign currency and that this will cause the exchange rate to go upward.